The Massachusetts Coastal Coalition’s Know Flood suite of services brings flood risk information to your fingertips. These services are designed to meet the needs of realtors, lenders, policy holders and residential and commercial applications where flood information can affect everyday life.

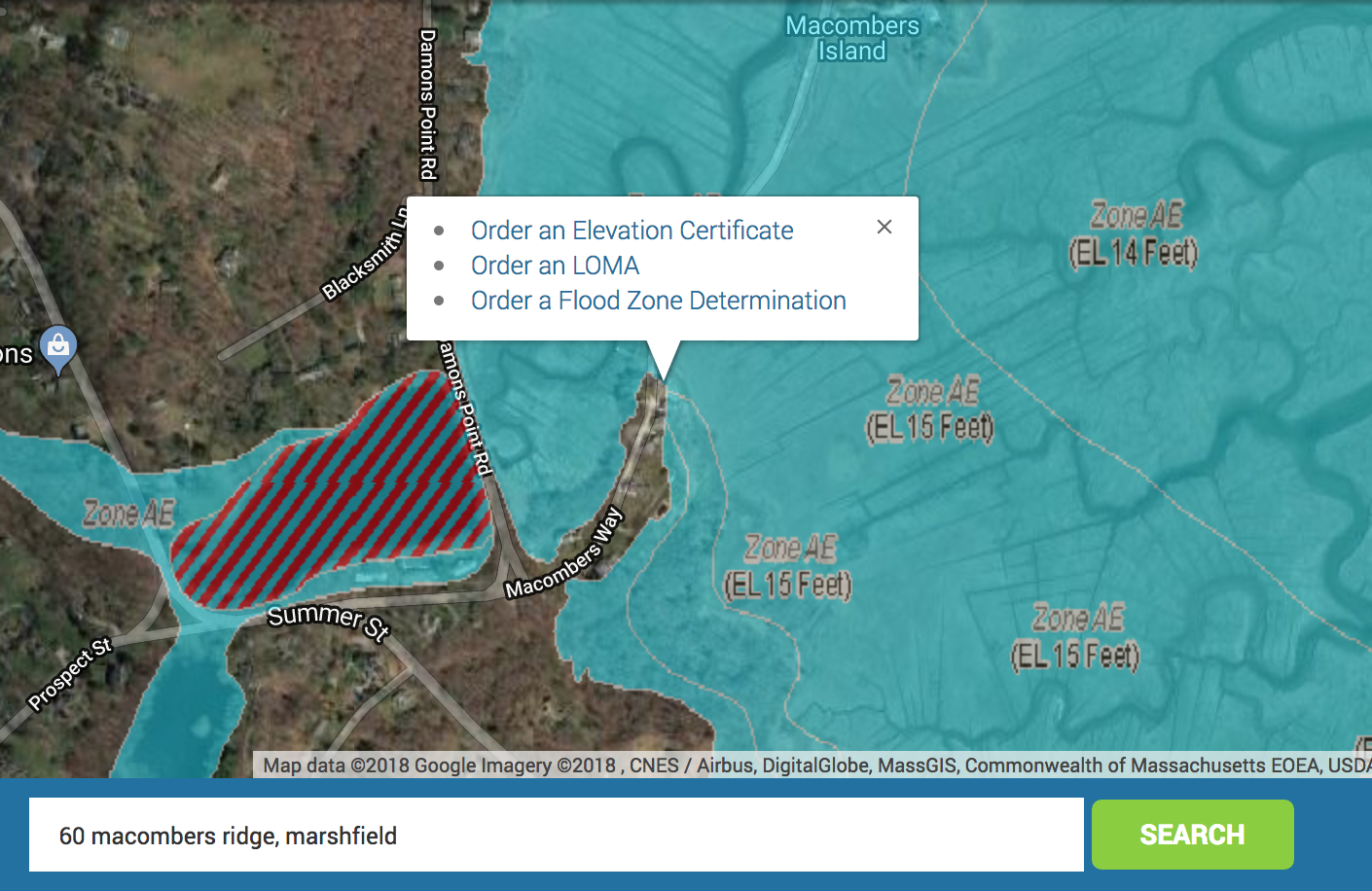

“Know Flood Mapping” Service Knowing your flood risk is now as easy as entering an address. The Know Flood Mapping Service has the entire nation’s digital flood maps online. Simply enter your address in the search bar, and the map pins your building’s location. This is available on our home page at www.knowflood.org

“Know Flood Zone” Determination The Know Flood Zone determination is a guaranteed product, which means we guarantee our accuracy to officially determine what flood zone you are in. This is the what lenders use to decide if you are “in or out” of the high risk flood zone. This is an ideal tool for real estate professionals looking to inform potential sellers and buyers. Along with our guaranteed determination comes our “Massive” report, which is one of the most comprehensive flood information reports available. It shows a map of your property, tells you the next closest flood zone, estimated ground elevation and more. All for one price.

“Know Flood Elevation” Certificate With our national network of land surveyors, we can offer standard prices for elevation certificates across the country. You can order and schedule your elevation certificate online and pick from a standard or a rush schedule.

“Know Flood Removal” LOMA The Letter Of Map Amendment (LOMA) is the easiest way to remove the building from the “A” or “V” zone if it qualifies. The Know Flood Removal is an expedited process and in most cases can be completed in 30 days. To start, you’ll need an elevation certificate. Then we review and verify that you are eligible. If you submit your LOMA request and are denied, there is no cost!

A portion of each service purchased is donated directly to the MCC. The MCC is a registered 501c3 charitable organization.

Before the start of 2018, many predicted political and economic uncertainty. This proved to be specifically true of the National Flood Insurance Program and the flood insurance market. In total, 2018 brought three program lapses lasting eight days and eighteen hours with seven short term extensions and a series of FEMA leadership and administrative changes. Predictions for 2019 bring with it additional uncertainty. With a new Congress, the introduction of a new rating system, and lending regulatory changes, 2019 could extend 2018’s flood insurance-related ebbs and flows.

When the new congress started in 2017, House Financial Services leadership announced that flood insurance reform would be a priority. At that time, the flood program was set to expire on September 30th of that year. Early on, several controversial reform bills were introduced that stalled in Congress. After the 2017 hurricane season hit, congress changed focus, leading to short term extensions of the flood program. In 2018, the short term extensions became more volatile leading to program lapses and week-long extensions. In 2019, there may be more short-term extensions, but there is also hope for true reform. On December 21st, Congress voted on a standalone bill to extend the NFIP to May 31st, 2019 setting up time for the new congress to develop long term reforms. Congresswoman Maxine Waters, who is set to be Chairperson of the Financial Services Committee, has already made flood insurance reform a committee priority. Broad goals such as improved mapping, affordability, and a long-term reauthorization for at least a five-year time period should help stabilize concerns about the flood program’s turbulence. However, if consensus is not reached by May 31st, more short terms extensions could plague the flood program.

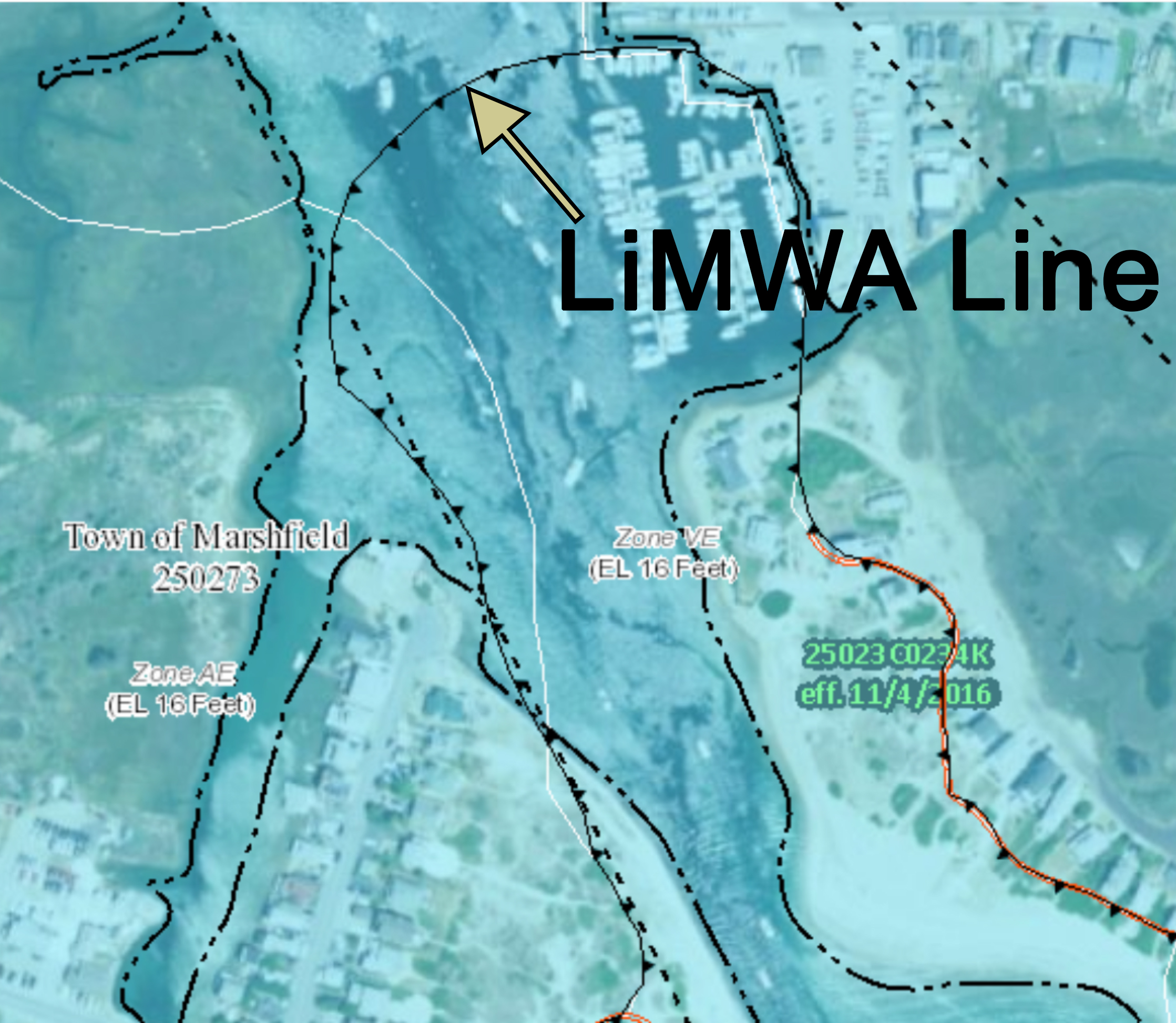

The term LiMWA has been mentioned with more frequency in recent months and depending on your location it could have an impact on your structure. LiMWA stands for Limit of Moderate Wave Action. A LiMWA, better known as a coastal A zone, and is an area on the Flood Insurance Rate Map where wave heights are calculated between 1.5 feet and 3 feet. While this may seem innocuous enough, LiMWA zones can be very important.

Over the past decade, post-storm damage surveys and laboratory tests have confirmed that wave heights as little as 1.5 feet can cause significant damage to structures that are not built to withstand such hazards. Therefore, LiMWA zones are areas that, for new and substantially improved structures, are required to be built to VE zone standards. This means requiring these structures to be elevated on piers, posts or piles. The only exception is stem wall foundations (foundations that are back filled inside). To complicate things further, construction code must meet “V” zone standards, while FEMA still rates these areas as an “A” zone.

Why does this matter to you? Right now, these zones in Massachusetts are not regulated. Meaning that you don’t have to build to “V” zone standards. However, in many other areas of the country they are regulated. Massachusetts, in all likelihood, will regulate these areas in the future. The map shows how the LiMWA is shown online. Know your zone, if you are in a LiMWA, and always try to exceed minimum standards.

Sue Sullivan is a top producing realtor for 15 years with Coldwell Banker in Scituate and is ranked as the top 15% of Coldwell Banker professionals worldwide for production and exceptional service. Susan became part of the MCC Board of Directors in 2016 to bring her expertise in real estate.

Sue’s Flood Real Estate Tips Keep your NFIP Policy In Place

As we enter 2019, its time to review your annual flood insurance policy. Review the policy coverage with your current insurer and question the deductible amount. Then it’s time to get a second opinion! I recently listed a home in an AE flood zone. The homeowner was paying $3,600 for an annual policy with a $2,000 deductible. This premium was high compared to homes in the immediate area. The property owner had not filed a flood damage claim in over 40yrs. After speaking with the insurer it was determined the property qualified for a deductible increase to the maximum amount of $10,000* (the maximum allowed for a 1-4 family building). This change reduced the annual flood policy to $2,200. Then the homeowner got a second opinion from an agency with flood insurance expertise; Murphy Carty Insurance. The original insurer was incorrectly designating the crawlspace as a basement, this significantly increased the annual cost of the policy. For the exact same FEMA coverage, they wrote the annual policy for $1,800! We all tend to pay our annual policies without reviewing or questioning them. This scenario will not always be the outcome but it is well worth exploring. You can ask to review your flood policy at any time, you do not have to wait until renewal. *Please note the homeowner had a mortgage on the property. In order to increase the deductible amount, they needed to obtain written permission from their lender. In this situation it was very easy to get the lender to agree.

NFIP Reverses Course In Limiting Sales

Right before the Government Shutdown on December 21st, Congress passed a 6 month extension of the NFIP. However, a legal decision on December 26th explained that because there was a government shutdown with no funding for DHS, FEMA also had to shut the NFIP down. This created massive chaos within all parts of the flood industry, as no new policies could be written, and no policies could be renewed. However, with extreme pressure from Congress and other industries and stakeholders, FEMA reversed their decision on December 29th restorative to December 21st.

NFIP Extented to May 31st

Multiple short extensions lead to 6-month extension December brought two short term extensions and a twelve-hour lapse to the NFIP. The lapse occurred when congress voted to extend the NFIP for a week, but the president had not signed the bill until noon time the next day. Finally, on December 20th, congress acted and voted to separate the NFIP from the appropriations bill and extend the NFIP to May 31st.

January 1st Changes

Preferred Risk Policies (PRPs): Premiums will increase 8 percent, with a total increase of 6 percent. Properties Newly Mapped into the SFHA: Newly Mapped policies are initially charged PRP premiums during the first year following the effective date of the map change. Annual increases to these policies result from the use of a “multiplier” that varies by the year of the map change; this multiplier is applied to the base premium before adding the ICC premium. As a result of increases to the multiplier that will be effective January 1, 2019, premiums for Newly Mapped policies will increase 15 percent, with a total increase of 11 percent.

Tim Carty owns MurphyCarty Insurance Agency, located in Scituate Harbor. His objective is to support policy holders, minimize their risk, and help navigate them through the flood program. Tim has an MBA from Boston University and an undergraduate from Babson College.

Tim’s Flood Savings Tips NFIP: Doesnt have to be expensive- Part 1

Flood insurance can be expensive: often times it is a tipping point for keeping a home, or deal breaker for considering the purchase of another. Simple ways to consider savings on the cost of flood coverage begin with an insurance agent who understands the complexities of writing flood insurance. Next is to determine if a policy is already in existence. In many cases, a policy has history that makes it a value relative to writing a new policy. Policies can always be reviewed for accuracy – many times policies are written against an older home where significant improvements have been made that might reduce the risk (and cost) of flood coverage. Policies can also be written with initial mistakes that are not realized: mistakes can happen and can cost insureds hundreds or even thousands of dollars per year. Deductibles can also be increased to reduce the cost of coverage. Contents coverage can be reduced or even eliminated. Dwelling coverage can be reduced to the level of a mortgage or home equity loan (whichever is higher) if an insured’s mortgage or loanable balance is below $250,000.

Stay tuned to Part 2 next quarter!

Note from the Chair

Last year was a challenging year for the NFIP, but a rewarding year for the MCC. We became an official 501c3 charitable organization, brought you our first ever services, and held our first ever post and pre disaster outreaches. 2019 will bring more rewarding changes such as a new grant program partnership, volunteer staff positions, and the finalization of a membership program. These are all aimed at bringing more awareness, assistance and information to those that we serve- you! We also have a seat at the table for some major changes with the NFIP in 2019, some of which are found in this newsletter. So stay tuned as we go for another wild ride in 2019.

Joe Rossi Chair and Executive Director Massachusetts Coastal Coalition